^^^Originally Posted by katya422

From ZH it looks like Silicone Valley was trying to reposition for this.

https://www.zerohedge.com/markets/30...banking-systemIn English? The bank had a lot of fixed-rate TSY (and other) exposure that was underwater and carrying an unrealized loss, and having concluded that rates will keep rising, the bank decided to restructure its assets and flip its portfolio from a fixed-rate one (where rate hikes cause even more capital losses) to a short-term one (where they lead to modest NIM gains). Of course, the transition ended up costing the bank billions.

In early 2009 US regulators suspended Mark to Market, and instead of having banks hold debt securities on their books at price, they allowed them to split their asset holdings into two components: Available for Sale (or AfS), a bucket which would be marked to market and which could be sold to short up liquidity, and Held to Maturity (or HTM), a (far larger bucket) which allowed the banks to keep debt securities at cost.

This was created to avoid cross-selling contagion if one bank was forced to liquidate securities and infect other holders of the same security. In other words, it was purely a idiosyncratic feature, not one that was meant to offset macro conditions. And understandably so: in a time of raging deflation, and ZIRP and QE, when rates would seemingly never go up, virtually nobody even considered a scenario when it would be the Fed itself that would force rates higher to fight galloping inflation.

Sadly for SIVB, that's where we are now, and the Fed's rate hikes have manifested in two ways.

- First, rising rates afford depositors a completely risk-free way of parking your money at Treasuries without taking on company-specific deposit risk. This is a big issue for SIVB because as noted above it has $170BN in deposits.

- Second, rising rates force the bank to sweep ever bigger losses on its debt assets under the rug. And yes, while the bank can hide behind the "held at cost" basis afforded by Held to Maturity, the fact that the bank's HTB book was of relatively moderate duration meant that even if it held to maturity, it would still suffer losses, which is why it proceeded with the previously discussed balance sheet restructuring.

The funny part, of course, is that we knew all of this!

To be sure, until recently nobody cared about net unrealized losses on bank portfolios because, well, there simply weren't any. But once the rate hikes started and debt prices - for anything from Treasurys, to MBS, to CRE - to started to tumble, the unrealized losses started to climb, and nowhere is this more visible than in Silicon Valley Bank's own balance sheet, where from virtually no losses a year ago, the number climbed to $16 billion as of Q3.

In some ways, SIVB was unique: while all US banks parked a chunk of their money in Treasuries and other bonds that dropped in value last year, SVB took it to a different level: its investment portfolio swelled to 57% of its total assets. No other competitor among 74 major US banks had more than 42%.

*******

And here lies the rub: if it was only SIVB that has an "unrealized loss" problem then there would be no contagion, and the rest of the banking sector would be safe and sound. Unfortunately, as explained, the reason why SIVB's HTM book blew up is because of surging rates, which is also why SIVB proceeded to liquidate its Available for Sale securities (at $26BN these are far less than the $91.3BN in HTM book). And it's also why every other bank is now suffering under the pressure of massive "net unrealized losses."

Just like SVB, the unrealized loss issue emerged only in 2022 when rates exploded and prices of debt securities tumbled. What stands out here is that while all banks have substantial exposure - the total is $250BN as of Dec 31, 22 - Bank of America has the most exposure at just under $110 billion.

And another problem: these amounts may not sound like a lot, but when expressed in terms of book shareholder value for any given bank, they are staggering.

Who else remembers Janet Yellen floating the idea of buying back US Treasuries from the banks?

So banks sitting on underwater assets + no body wants to take out new loans because interest rates are so high = this seems bad.

|

|

Results 31 to 60 of 285

-

03-10-2023, 11:23 AM #31No Huevos

- Join Date: Dec 2011

- Location: United States

- Posts: 20,098

- Rep Power: 363947

INTP Crew

INTP Crew

Inattentive ADD Crew

Mom That Miscs Crew

-

03-10-2023, 11:24 AM #32Registered User

- Join Date: Aug 2009

- Posts: 34,956

- Rep Power: 366267

lol at “Banks make money off of loans”.

The amount of money they make on even higher interest accounts is nothing compared to the money they make by investing everyone’s money in high yield compounding interest accounts.

This is the point of escrow and why you company will always wait as long as legally possible to pay you.

They use their customers money to make money.I only read thread titles and my own posts.

cVc (OIF/OEF): *Retired*

Sorry for perfect english; I have a degree.

“The stories and information posted here are artistic works of fiction and falsehood. Only a fool would take anything posted here as fact.“

PS: Don't eat poop, just don't let the idea of it stop you from living life to its fullest.

-

-

03-10-2023, 11:30 AM #33Anti-Circumcision

- Join Date: Aug 2009

- Location: Franklin, Indiana, United States

- Posts: 61,627

- Rep Power: 214511

And this is why the fed waiting so long to start hiking was ****ing retarded. It's kind of amazing how bad our leadership is at leading. They should have been running quarterly 25 basis point hikes for years. Very slow very steady giving everyone time to reposition assets.Originally Posted by XterraRob

*PUREBLOOD CREW*

*DAD CREW*

*SUPER STRAIGHT*

*NATURAL DICK CREW*

*CCW*

-

03-10-2023, 11:35 AM #34No Huevos

- Join Date: Dec 2011

- Location: United States

- Posts: 20,098

- Rep Power: 363947

A bank is a little different than some other type of company.Originally Posted by Ironmanlet

Believe it or not, they don't actually have to have any money to create a loan. There used to be a reserve requirement, so e.g. they could make $10 in loans for every $1 in deposits. But that little wrinkle was smoothed out.

They create the money by lending it to you. They profit be demanding you return more money to them than what they have lent out to you [interest].

For quite a while now the banks haven't had any reason to care really about accruing and holding consumer deposits. They have been charging people various fees for the privilege of having a checking or savings account and paying nearly no interest to depositors.INTP Crew

Inattentive ADD Crew

Mom That Miscs Crew

-

03-10-2023, 11:50 AM #35Registered User

- Join Date: Apr 2012

- Location: Alberta, Canada

- Age: 39

- Posts: 26,409

- Rep Power: 240411

Wealth needs to be destroyed for inflation to be conquered, allowing people to just move assets around won't help there.Originally Posted by JoshSP1985

The Fed giveth and the Fed taketh away. Money is merely a unit of exchange allowing quick trade in a capitalist economy designed to continue pushing us further and further forward by creating and improving upon the products/services we all need.

-

03-10-2023, 11:50 AM #36No Huevos

- Join Date: Dec 2011

- Location: United States

- Posts: 20,098

- Rep Power: 363947

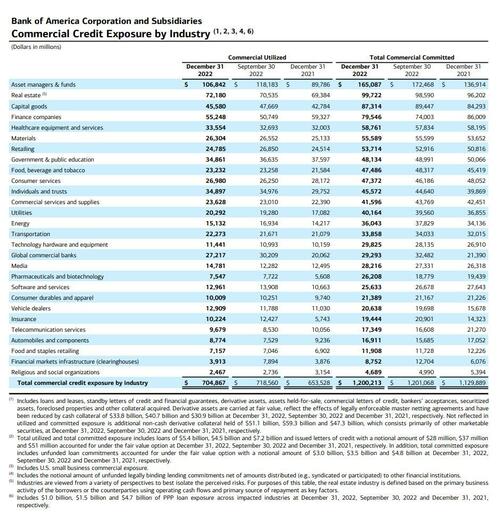

Oh and about Bank Of America:

B of A Commercial Credit Exposure By IndustryBank of America's unrealized loss (i.e., the market-value gap between its HTB book and fair value) represents 43% of combined total equity

Poor management rating likely placed a large bank on FDIC's 'problem bank' list

Was it B of A?

https://www.spglobal.com/marketintel...-list-69475896INTP Crew

Inattentive ADD Crew

Mom That Miscs Crew

-

-

03-10-2023, 12:33 PM #37No Huevos

- Join Date: Dec 2011

- Location: United States

- Posts: 20,098

- Rep Power: 363947

May be totally unrelated, but that timing though.

Link: https://www.zerohedge.com/markets/we...g-transactionsINTP Crew

Inattentive ADD Crew

Mom That Miscs Crew

-

03-10-2023, 12:36 PM #38Floridayyy

- Join Date: Sep 2007

- Location: Turks and Caicos Islands

- Posts: 9,170

- Rep Power: 155617

And they get their buttbuddies in DC/the federal reserve to print off a few $billy as needed tooOriginally Posted by Ironmanlet

Coincel

Florida crew (lol at coldcels)

-

03-10-2023, 12:37 PM #39Registered User

- Join Date: Apr 2012

- Location: Alberta, Canada

- Age: 39

- Posts: 26,409

- Rep Power: 240411

Zerohedge can get fukked

-

03-10-2023, 12:38 PM #40Forever Santa

- Join Date: Dec 2012

- Posts: 26,299

- Rep Power: 449943

Fuk is it over for us Wells Fargo celsOriginally Posted by katya422

-

-

03-10-2023, 12:43 PM #41Registered User

- Join Date: Oct 2019

- Age: 54

- Posts: 27,284

- Rep Power: 107638

its never your money

HTC is too skinny for me. Fat Girls only crew. serious

Chubby Chaser and Fat Girls Only crew Founder

-

03-10-2023, 12:49 PM #42Silent Hill Brah

- Join Date: Apr 2006

- Location: Maryland, United States

- Age: 35

- Posts: 6,208

- Rep Power: 44053

I'm supposed to close on a house in less than a month. Did I dun goof?Originally Posted by Train57

.:MiscMarioBrahs:.

**Misc Cologne Crew**

**Raw Denim Crew**

-

03-10-2023, 12:53 PM #43No Huevos

- Join Date: Dec 2011

- Location: United States

- Posts: 20,098

- Rep Power: 363947

Not @ me, but:Originally Posted by AvengeMe

- do you like the house?

- good location?

- could see yourself living there...like for a long time maybe?

- can you afford it without being "house poor"?

Yes to all of the above? I think you are fine. Have to live someplace.

I mean maybe home prices will go down where you live, but if mortgage interest increases and you can't buy for cash that could be a wash. And you can sleep inside your house, get out of the weather, store you belongings...paper investments not so much.INTP Crew

Inattentive ADD Crew

Mom That Miscs Crew

-

03-10-2023, 01:01 PM #44Silent Hill Brah

- Join Date: Apr 2006

- Location: Maryland, United States

- Age: 35

- Posts: 6,208

- Rep Power: 44053

Yes to all of the above so that's good at least. Mortgage is a bit high since it's a 15 year but wouldn't say I'll be house poor.Originally Posted by katya422

.:MiscMarioBrahs:.

**Misc Cologne Crew**

**Raw Denim Crew**

-

-

03-10-2023, 02:51 PM #45Banned

- Join Date: Jan 2023

- Age: 54

- Posts: 1,188

- Rep Power: 0

Techies on suicide watch

Tradies Win again

-

03-10-2023, 03:53 PM #46Registered User

- Join Date: Oct 2011

- Age: 38

- Posts: 18,889

- Rep Power: 48017

I am 50% potato so please explain

Customer wants a mortgage

Bank writes mortgage and house is paid for by bank

Now customers pays back at blank interest

Interest rate jumps

Why would it matter what current interest rate is for a bank on money they lent out 10-15-20 years ago?**Black out tape over all laptop/cell phone cameras so gov cant spy on me fapping crew**

-

03-10-2023, 04:20 PM #47No Huevos

- Join Date: Dec 2011

- Location: United States

- Posts: 20,098

- Rep Power: 363947

I don't believe mortgages are specifically the problem here, but could be part of it. The Federal Reserve bought a lot of mortgages and I don't believe they have offloaded too much of that.Originally Posted by helpmee

It's more about banks being loaded up with investments which are paying a return below the rate of inflation and below the current interest rates.

A little like if you have a salary of $75K a year and you are feeling fine...covering expenses, doing some investing. But then your expenses increase [bank: buildings, utilities, staff] so to still be in a good position you need to increase your income.

For banks that would mean moving from low yield investments to higher yield investments, or at least adding more high yield products.

Except that with interest rates being so high no one [well most people] wants to take on more debt and pay so much for the bank's money.

Yeah, the really big guys have stuff like revolving consumer credit which they can really hike up rates on, but that debt is also non-secured and more liable to default.

From what I've read today this is a bigger problem for the smaller regional banks vs. the very big nationwide banks because though the big banks have been excused from meeting any reserve requirements the smaller regional banks are still reserve constrained. The big banks are loaded with cash and have been getting a nice rate of return from the Fed.

I'm just watching a short video about what happened to a lot of regional banks today- stocks hit hard, trading halted, possible that some restructuring will happen over the weekend...bank holiday?

Listed:

- First Republic Bank

- Signature Bank

- Pac-West Bancorp

- Western Alliance Bancorp

First Republic went from $123 to $86 per share IIRC.

Says that someone high up at SVB bank sol a lot of their stock holdings 2 weeks ago. Claims he got a call that there is a run on withdrawals from Signature Bank.INTP Crew

Inattentive ADD Crew

Mom That Miscs Crew

-

03-10-2023, 04:46 PM #48No Huevos

- Join Date: Dec 2011

- Location: United States

- Posts: 20,098

- Rep Power: 363947

For anyone following the story this is a list of banks with exposure risk to SilverGate, the crypto bank that recently went under.

INTP Crew

INTP Crew

Inattentive ADD Crew

Mom That Miscs Crew

-

-

03-10-2023, 05:25 PM #49No Huevos

- Join Date: Dec 2011

- Location: United States

- Posts: 20,098

- Rep Power: 363947

News of companies with accounts at SVB beginning to emerge.

Link: https://twitter.com/BrianRoemmele/st...216444931?s=20

Link: https://twitter.com/WallStreetSilv/s...964784130?s=20

Link: https://twitter.com/WallStreetSilv/s...792014337?s=20

Will banks outside the US be in worse shape?

Link: https://twitter.com/BankerWeimar/sta...135478278?s=20

And a little comic relief.

INTP Crew

INTP Crew

Inattentive ADD Crew

Mom That Miscs Crew

-

03-10-2023, 05:29 PM #50Registered User

- Join Date: Apr 2012

- Location: Alberta, Canada

- Age: 39

- Posts: 26,409

- Rep Power: 240411

-

03-10-2023, 05:31 PM #51Banned

- Join Date: Jan 2023

- Age: 54

- Posts: 1,188

- Rep Power: 0

No idea what that is but lol @ keeping your coins in a ****ing bankOriginally Posted by katya422

-

03-10-2023, 05:33 PM #52No Huevos

- Join Date: Dec 2011

- Location: United States

- Posts: 20,098

- Rep Power: 363947

Originally Posted by Destor

More:

Link: https://twitter.com/wbhoban/status/1...219475457?s=20INTP Crew

Inattentive ADD Crew

Mom That Miscs Crew

-

-

03-10-2023, 05:35 PM #53No Huevos

- Join Date: Dec 2011

- Location: United States

- Posts: 20,098

- Rep Power: 363947

INTP Crew

INTP Crew

Inattentive ADD Crew

Mom That Miscs Crew

-

03-10-2023, 05:45 PM #54No Huevos

- Join Date: Dec 2011

- Location: United States

- Posts: 20,098

- Rep Power: 363947

So is this good since the FDIC should be able to cover the loss, or bad because so many depositors could be really screwed?

Correction: should say that 97.3% of depositors have some level of uninsured exposure.INTP Crew

Inattentive ADD Crew

Mom That Miscs Crew

-

03-10-2023, 05:45 PM #55Registered User

- Join Date: Mar 2014

- Location: Texas, United States

- Age: 35

- Posts: 6,121

- Rep Power: 55586

I work on an active trade line for a large broker, and our Teams chat was all over the place today. Interesting stuff. Sat back and watched. A few clients who were spooked but most of today was business as usual.

Being anti-2nd Amendment is like saying "We have too many rights, please take some away!"

-

03-10-2023, 05:51 PM #56No Huevos

- Join Date: Dec 2011

- Location: United States

- Posts: 20,098

- Rep Power: 363947

It is just hard to say at this point how bad the knock on effects may be to other banks and customers of SVB. The corporate customers have 4 business days to disclose, though a lot may come out before then.Originally Posted by Firefightn24

Another contagion chart...this one from Bloomberg instead of WSJ:

A lot of uninsured deposits:

From 2022:

Last edited by katya422; 03-10-2023 at 06:00 PM.

INTP Crew

Inattentive ADD Crew

Mom That Miscs Crew

-

-

03-10-2023, 05:53 PM #57Registered User

- Join Date: Mar 2016

- Location: United States

- Posts: 342

- Rep Power: 12124

Really, really bad. This reeks of 'too big to fail'. And with the conflict of interest with the CEO, I thought they were supposed to tighten up oversight on that kind of thing after '08. Shoot...Originally Posted by katya422

-

03-10-2023, 06:07 PM #58No Huevos

- Join Date: Dec 2011

- Location: United States

- Posts: 20,098

- Rep Power: 363947

Sharing stuff as I find it...

Link: https://twitter.com/Mayhem4Markets/s...396315137?s=20

I guess this could be one possible resolution. Fed fixing to buy a bank???

INTP Crew

INTP Crew

Inattentive ADD Crew

Mom That Miscs Crew

-

03-10-2023, 06:13 PM #59Registered User

- Join Date: Jun 2011

- Posts: 14,748

- Rep Power: 56524

Less news, more what this will mean consequence wise and what actions are best to take.

Thanks2014 Misc Resolution: Negging no pics (screen captures of text don't count as pics)

HairyWBush Reps for life - Hamster Compassion: https://forum.bodybuilding.com/showthread.php?t=181804893

-

03-10-2023, 06:13 PM #60No Huevos

- Join Date: Dec 2011

- Location: United States

- Posts: 20,098

- Rep Power: 363947

3rd Bank Coming Soon?

Some votes for Wells Fargo.

Link: https://twitter.com/theRealKiyosaki/...294640641?s=20INTP Crew

Inattentive ADD Crew

Mom That Miscs Crew

Bookmarks